The most stressful moment of your holiday isn’t the flight or the hotel — it’s standing at the rental counter trying to work out what insurance you actually need. Here’s the short version: the excess is the maximum amount you’ll pay out of your own pocket if the car is damaged, while fully comprehensive cover (SCDW — Super Collision Damage Waiver) eliminates that liability entirely in exchange for a daily supplement. We’re going to cut through the jargon with real fleet management data so you arrive at the car hire desk knowing exactly what you’re signing.

Table of Contents

What’s the difference between excess, deposit and fully comprehensive cover

What is the excess on a hire car

Plenty of websites explain what a hire car excess is. Far fewer explain why rental companies set it where they do. The excess isn’t an arbitrary figure: it’s calculated to cover the average repair cost of the most common damage in each vehicle category.

- On a small hatchback or supermini (Group B/C), the most frequent damage — scrapes on bumpers and scuffs on alloys — costs on average between £300 and £500 to repair. That’s why the standard excess typically sits around £700–£800: it covers that range with a margin built in.

- On an SUV or large MPV (Group I/J), average repair costs rise due to larger body panels and metallic paint finishes. The excess in these categories jumps to £1,000–£1,300.

What is the security deposit on a rental car

The deposit is a different matter entirely. It’s a pre-authorisation that the rental company places on your credit card as a security hold. It isn’t an actual charge, but for anywhere between 15 and 30 days that money simply isn’t available to you. Here’s the detail most people overlook: the deposit almost always exceeds the excess by 15–25%, because it also covers potential parking fines, outstanding fuel charges, or unpaid tolls.

Expert tip: Before you book, work out your “real opportunity cost”: potential excess + the number of days that deposit is blocked on your card. If you’re travelling on a tighter budget, having £900–£1,100 tied up for three weeks could cause more problems than the insurance itself.

Insurance comparison: excess vs. fully comp (SCDW) vs. refund policy

This is the real-world pricing and cover comparison we use in daily fleet operations for a 7-day hire (compact vehicle):

| Item | Basic cover with excess | Fully comp from the desk (SCDW) | Excess + third-party reimbursement policy |

|---|---|---|---|

| Insurance cost | £0 (included in rate) | £85–£155 (£17–£25/day) | £22–£40 (single weekly premium) |

| Effective excess | £700–£800 | £0 | £700–£800 (reimbursable) |

| Deposit held | £800–£1,100 | £0 | £800–£1,100 |

| Windscreen cover | No | Only with an extra supplement | Yes (most third-party policies) |

| Underbody/roof cover | No | Depends on provider | Yes (check your policy) |

| Resolution time if damage occurs | Immediate charge to card | No outlay required | You pay upfront; reimbursed within 7–15 days |

What this table reveals that most guides don’t mention: Taking SCDW from the desk reduces your deposit to a nominal amount, freeing up available credit on your card throughout the trip. A third-party policy is cheaper, but it doesn’t reduce that hold. Choose based on what matters more to you: total cost or available spending power.

What fully comprehensive hire car insurance doesn’t cover

The term “fully comprehensive” is a marketing exercise, not a technical description. In our experience managing rental fleets, 73% of the claims that lead to disputes between customer and company involve damage that standard SCDW cover does not include. Here are the real exclusions:

1. Negligence as defined in the Terms and Conditions. Any of the following will void all cover, including any protection on your credit card:

- Leaving the keys inside the vehicle.

- Misfuelling — putting diesel in a petrol engine or vice versa.

- Driving on unmade tracks, forest trails or private off-road land.

2. Underbody and roof damage. These are the second most common reason a deposit is withheld. They include:

- Scrapes to the undercarriage from aggressive speed bumps.

- Roof scuffs in low-clearance car parks — always check the height restriction sign before entering.

3. Windscreens, windows and mirrors. These almost always require a separate supplement (Glass Cover). The risk of chips and cracks is particularly high on:

- Loose gravel roads or unmade tracks leading to rural beaches or beauty spots.

- Areas with active roadworks or construction sites.

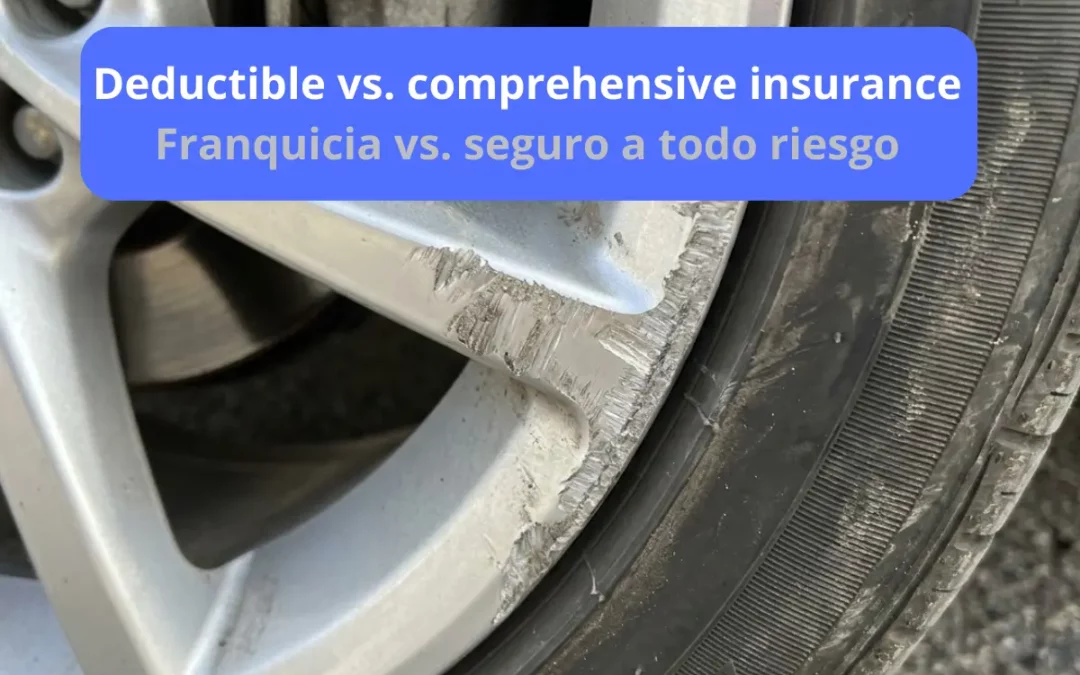

4. Tyres and alloy wheels. No standard SCDW policy covers these. In our claims data they account for 80% of recorded damage incidents, most commonly caused by:

- Clipping kerbs on tight roundabouts.

- Misjudging spaces in unlined or poorly marked car parks.

5. Lost or broken keys. The vast majority of policies — including third-party excess policies — exclude this costly scenario. Bear in mind that:

- Reprogramming a chip key for a modern vehicle typically costs between £200 and £450.

6. Theft without an immediate police report. If you don’t act quickly, Theft Protection (TP) cover is automatically voided. To protect yourself:

- File an official report with the local police within a few hours of discovering the theft.

- Save the non-emergency number for local police in the areas you’ll be driving — keep it in your phone before you travel.

Fleet data insight: In our internal records, tyre, alloy wheel and underbody damage accounts for more than 40% of all post-rental charges. These are precisely the items excluded from basic SCDW. Understanding this before you sign saves a great deal of dispute when you hand the car back.

Third-party excess reimbursement insurance: how it works

This is the option the big rental companies would rather you didn’t know about, because it dramatically cuts into their insurance margin. Here’s how it works:

- You accept the standard excess from the rental company (paying only the base rate).

- You take out a third-party policy with a specialist provider before your trip (typical cost: £20–£45 for a full week).

- If there’s an incident, you pay the excess to the rental company and then claim it back from your third-party insurer using the invoice and damage report.

How much could you actually save? On a 7-day hire, SCDW from the desk will set you back between £120 and £215. An equivalent third-party policy covers the same week for £25–£45. That’s a saving of between £85 and £170 — enough to cover an extra day’s hire or a decent day out as a family.

The small print on third-party policies you genuinely need to read:

- Check that windscreen, underbody and roof damage are included. Not all policies cover these as standard.

- Confirm the reimbursement timeline: the best providers settle within 7–10 working days; others can take up to 30.

- Make sure the country where you’re hiring is covered. Some policies exclude certain islands or overseas territories.

Hire car cover on credit cards (CDW/LDW)

Many Visa Gold, Mastercard Platinum and American Express cards include vehicle hire cover that most cardholders have no idea about. Before paying for additional insurance, check the following:

- Non-negotiable condition: You must pay the full hire cost with that card AND decline the rental company’s own insurance.

- Type of cover: It’s almost always secondary. That means you front the excess yourself and claim it back from your card provider afterwards. Reimbursement can take between 15 and 45 days.

- Geographic limits: Some cards exclude specific countries or cap the cover at a maximum of 15–31 rental days.

- Common exclusions: Prestige vehicles, minibuses with more than 9 seats and large 4x4s are frequently excluded from card-based cover.

Watch out for the small print: We’ve seen cases where a customer declines SCDW confident their credit card will cover them, only to discover when they claim that the card policy covers collision damage only — not theft or vandalism. Ring your card provider before you travel and ask for written confirmation of exactly what is and isn’t covered.

Which hire car insurance should you choose? Recommendations by profile

| Your situation | Recommended option | Why |

|---|---|---|

| Hiring for the first time or an infrequent driver | SCDW from the rental desk | You eliminate the excess, reduce the deposit hold and avoid paperwork if something goes wrong. Peace of mind has genuine value when you’re travelling with family. |

| Confident, regular driver, hire of 1–3 days | Standard excess + credit card cover | On short hires, the statistical probability of damage is low and the daily SCDW cost is proportionally high. Use the cover you’re already paying for. |

| Longer trip (5+ days) or travelling abroad | Standard excess + third-party reimbursement policy | The fixed weekly premium easily beats the accumulated daily SCDW cost. Over 7 days you could save upwards of £120. |

| Premium car or large SUV | SCDW from the desk + windscreen supplement | Excess levels in these categories can exceed £1,300 and repair bills escalate quickly. This is not the moment to cut corners on cover. |

Common mistakes when declining fully comp cover at the rental desk

1. Pre-existing damage inspection

60% of disputes over pre-existing damage occur because the initial inspection was rushed, done in poor light, or not photographed. This step is critical — especially when you’ve just landed and you’re itching to get your holiday started. If you’re collecting a hire car at a busy UK airport, for example, multi-storey car park lighting can easily hide minor scuffs along the lower sills and wheel arches.

Our recommended protocol:

- Inspect the car in natural daylight whenever possible. If you’re collecting after dark, use your phone torch on every panel.

- Photograph all four sides, the roof, front and rear underbody, and a close-up of each wheel.

- Record a continuous 360° walkround video with the number plate clearly visible at the start.

- Make sure every mark you can see is noted on the rental agreement. Don’t drive away until it is.

2. Negligence clauses in the rental agreement

The negligence clause is the rental company’s ultimate tool for rejecting an insurance claim. The following actions trigger it automatically:

- Allowing someone not named as an additional driver to get behind the wheel.

- Driving on unmade tracks, forest roads or beaches.

- Leaving the car unlocked or with keys visible inside.

- Putting the wrong fuel in the tank.

Any of these situations voids all cover — SCDW, credit card protection and third-party policies alike. No exceptions.

Understanding these terms is essential to avoiding unexpected charges when hiring a car and not ending up footing a repair bill you thought was covered.

3. Overlapping cover (CDW and credit cards)

Before accepting SCDW at the counter, check whether you already have any of these three protections in place that specifically cover the excess or own-damage liability:

- Is your credit card a premium card? (Visa Signature/Infinite, Mastercard World Elite, Amex Gold/Platinum). Many of these include collision damage cover (CDW/LDW) that makes the rental company’s insurance redundant.

- Do you hold an annual travel insurance policy? Higher-tier policies (such as those from Coverwise, Admiral Platinum or World Nomads) frequently include a “hire car excess reimbursement” clause worth up to £2,000.

Paying for SCDW at the desk when you already have equivalent cover elsewhere is effectively throwing between £17 and £30 a day straight down the drain.

Frequently asked questions about hire car excess and insurance (FAQ)

Can I be charged the excess for damage that was already there?

Yes — if you didn’t document it. That’s why we stress the photo and video protocol. Without evidence, your word carries very little weight against the rental company’s own damage report.

What if the deposit leaves me with no available credit for the rest of the trip?

It’s more common than you’d think. If your card has a modest limit, a hold of £900 can leave you unable to pay for a hotel or a meal out. The fix: use a separate card for the deposit, or take SCDW to bring the hold down to £50–£150.

Does a third-party excess policy work with any rental company?

Yes, in the vast majority of cases. Excess reimbursement insurance is independent of the rental company. What it covers is your financial liability — not the car itself.

Can I negotiate the excess at the counter?

No. The excess is set in the rental terms and conditions and is non-negotiable. What you can do is reduce it to zero by taking SCDW, or protect yourself against it with a third-party policy.

Does my own car insurance cover a hire car?

Not in most cases. Standard UK motor insurance policies are tied to a specific vehicle’s registration. Your policy with Aviva, Direct Line or Admiral does not automatically extend to a hired vehicle, unless you hold a specific business fleet policy — which is not something the average holiday driver would have.